Business/Economic Cycle

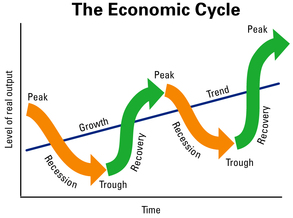

Business Cycle: Expansion(lots money, low unemployment, spending high) – recession (slows, more unemployment, less spending) – depression (prolonged recession) – recovery (spending again, unemployment lowers) OA 2 Explain the concept of economic resources (e.g., land, labor, capital, entrepreneurship)

OA 3 Describe the concepts of economics and economic activities Basic economic problem? (oa3) Unlimited wants for limited resources. Scarcity: A condition in which more goods and services are desired than are available. Opportunity cost: The value of what is given up when an economic choice is made. Three economic questions? (oa3) 1. Which goods and services should be produced? 2. How should the goods and services be produced? 3. For whom should the goods and services be produced?

OA 5 Explain the principles of supply and demand

Supply: The amount of goods producers are willing to produce and sell at a given price. Demand: The amount of goods consumers are willing and able to buy at a given price. Elasticity: The degree to which changes in price affect the demand for a product. Elastic demand: Changes in the price of the product result in changes in demand for that product. Inelastic demand: Changes in the price of the product have very little effect on the demand for that product. Demand? Affecting factors? -relationship between quantity of a product consumers are willing and able to purchase and the price

Supply? Affecting factors? -relationship between quantity of a product producers are willing and able to purchase and the price

Law of Demand: When the price of a product is decreased, the demand for the product increases. When the price of a product increases, the demand for the product decreases. Law of Supply: When the price of a product is increased, more will be produced. When the price of a product is decreased, less will be produced. The supply of a good or service:Increases when demand is great. Decreases when demand is low. Market Price? Equilibrium... - the interception of supply and demand Equilibrium: Point at which consumers buy all of a product that is supplied, leaving neither a surplus nor a shortage What is Supply? What is Demand? What is equilibirium? Price goes up - demand goes down Price goes down - demand goes up Price goes up - supply goes up Price goes down - supply goes down Supply is the relationship between the quantity of a product that producers are willing and able to provide and the price. Demand is the relationship between the quantity of a product consumers are willing and able to purchase and the price. Profit is also an important aspect since producers need to make money. OA 10 Explain the concept of competition

|

Difference between macro- and micro- economics?

Macroeconomics studies economic behavior and relationship of the entire society. Microeconomics examines relationships between individual consumers and producers. OA 1 Distinguish between economic goods and services A good is something you can touch, and a service is something someone else does for you. Economic goods - a commodity or service that can be utilized to satisfy human wants and that has exchange value Economic services - are activities that the buyer does not obtain exclusive ownership. These activities mainly deal with resources, experience and skills Products - both goods and services FOUR IMPORTANT QUALITIES OF SERVICES THAT ARE NOT SHARED BY PRODUCTS.

OA 4 Determine forms of economic utility (e.g., time, place, possession) created by marketing activities UTILITY: amount of satisfaction a consumer receives from the consumption of a product or service. ADDED VALUE Form utility: Usefulness provided by changing raw materials or assembling parts to create a useful good. EX - PUTTING BIKE TOGETHER FOR YOU AT WALMART Place utility: Usefulness provided by having a product available where customers need it. BEING ABLE TO BUY BIKE AT STORE OR ONLINE Time utility: Usefulness provided by having a product available when it is needed. HAVING BIKES AVAILABLE AT CHRISTMAS OR SUMMER Possession utility: Usefulness provided by creating opportunities for the consumer to own the product. I CAN PAY FOR BIKE WITH CHECK, CREDIT CARD, LAYAWAY, ETC... Information utility: Usefulness provided by communicating information about products. ADS, COMMERCIALS, FLYERS, SIGNS, DISPLAYS,ETC... OA 6 Explain the types of economic systems (e.g., capitalism, socialism, communism)

Command economies- where a central authority makes the key economic decisions. Mixed economies- contain both private and public enterprises. OA 7 Determine the role of government (e.g., regulator, provider of services, competitor, supporter) in business 1. provider of services - schools, roads, security, subsidies 2. regulator - laws designed to protect health, safety, and welfare -

3. Supporter - help businesses get loans - SBA - small business association - help with college loans, etc... 4. Competitor - US postal service OA 8 Explain the concept of private enterprise Profit: Money left after all the expenses of a business have been deducted from the income Making a profit is a primary incentive of the free enterprise system. It is one way of measuring success in a free enterprise system. Characteristics? - based on independent decisions by businesses and consumers with only a limited government role regulating those relationships

OA 11 Explain measures used to analyze economic conditions (e.g., gross domestic product, inflation, employment rate) -Productivity: output per worker hour, measured over period of time. -Gross National Product: GNP. dollar value of goods or services produced by a nation -Gross Domestic Product: GDP. output of goods or services produced by labor and properly located within a country -Customer Price Index: CPI. measures change in price over a period of time of some specific retail goods or services. -Producer Price Index: PPI. measures wholesale price levels in the economy. -Standard of Living: quality of goods and services that a nation's people have -Unemployment Rate: rate at which people at a job are layed off or fired

PRODUCTIVITY |

Econ Vocab

Patent: A legal document that gives an inventor the sole right to produce, use, and sell an invention. A patent lasts for 20 years. During this period, no business or individual can copy or sue the patented invention without the patent holder’s permission.

Copyright: Protects original works of an author. (e.g., music, books, computer software.) A copyright lasts for 70 years after the death of the author.

Trademark: Word, symbol, design, or combination of these that a business uses to identify itself or something

economic measurements: measures a

country’s strength (financially)

Goals of a healthy economy: increase productivity, decrease unemployment,

and maintain stable prices (no inflation)

International trade: trading products

with other countries

import - things we buy from other countries

exports – things that we sell to other countries

absolute advantage: country has all thenatural resources and talents to trump all the other countries in the

production of a product – china and silk

Benefits of international trade: lower

prices, allies, higher employment

trade barriers

Global Marketing strategies:

Non price competition – companies compete

with quality, service, luxury – anything other than price

Price competition – competitors keep up

with each other’s prices

Monopoly – NO competition – (illegal) When a company controls all of a market. There is no competition.

oligopoly – legal monopoly – cable, us mail, etc…

Profit = Revenue (sales)– Expenses (costs)

what is an industry? Collection of

business in a category – food, car, fashion, tech, etc…

Patent: A legal document that gives an inventor the sole right to produce, use, and sell an invention. A patent lasts for 20 years. During this period, no business or individual can copy or sue the patented invention without the patent holder’s permission.

Copyright: Protects original works of an author. (e.g., music, books, computer software.) A copyright lasts for 70 years after the death of the author.

Trademark: Word, symbol, design, or combination of these that a business uses to identify itself or something

- Economy - makes decisions to answer three basic economic questions What to produce, For whom, and how to produce it

- Risk - potential loss

- Consumer - uses the product

- Customer - buys the product Competition - struggle for customers

- Monopolies - illegal because they prevent competition

- Don't forget ... Scarcity Opportunity cost Goods services needs wants In elastic Supply and demand Factors of production aka economic resources Types of economies Imports exports tariff quota embargo Benefits of marketing Forms of business organization Equilibrium Price and no price competition Business cycle

economic measurements: measures a

country’s strength (financially)

Goals of a healthy economy: increase productivity, decrease unemployment,

and maintain stable prices (no inflation)

International trade: trading products

with other countries

import - things we buy from other countries

exports – things that we sell to other countries

- Trade surplus - export more than importing

- Trade defect - import more than export

absolute advantage: country has all thenatural resources and talents to trump all the other countries in the

production of a product – china and silk

Benefits of international trade: lower

prices, allies, higher employment

trade barriers

- tariff: tax on imports

- quota: number limits

- Embargo: ban

Global Marketing strategies:

- globalization: same product same promo everywhere (internationally)

- adaptation: change mkt strategies to meet the needs of target market

- Customization: new plan and new product for new people

Non price competition – companies compete

with quality, service, luxury – anything other than price

Price competition – competitors keep up

with each other’s prices

Monopoly – NO competition – (illegal) When a company controls all of a market. There is no competition.

oligopoly – legal monopoly – cable, us mail, etc…

Profit = Revenue (sales)– Expenses (costs)

what is an industry? Collection of

business in a category – food, car, fashion, tech, etc…

ECONOMIC PRINCIPLES

OA1

Distinguish between economic goods and services

OA2

Explain the concept of economic resources (e.g., land, labor, capital, entrepreneurship)

OA3

Describe the concepts of economics and economic activities

OA4

Determine forms of economic utility (e.g., time, place, possession) created by marketing activities

OA5

Explain the principles of supply and demand

OA6

Explain the types of economic systems (e.g., capitalism, socialism, communism)

OA7

Determine the role of government (e.g., regulator, provider of services, competitor, supporter, protection agencies) in business

OA8

Explain the concept of private enterprise

OA9

Identify factors (e.g., economics, human, nature) affecting a business's profit

OA10

Describe ways competition affects business decisions

OA11

Explain measures used to analyze economic conditions (e.g., gross domestic product, inflation, employment rate)