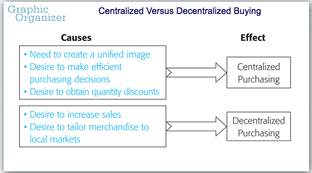

OB 4 Compare and contrast types of buying methods (e.g. resident buying, centralized buying, decentralized buying

centralized buying - when buying for all locations done centrally from home office decentralized buying - authority to purchase goods is given at the store level resident buyer - individual with an office in an important merchandise center. A resident buyer is crucial to providing valuable merchandising information and allows a company to keep in close touch with the market. A resident buyer can be inside or outside the organization. organizational buyer One who purchases goods for business purposes, usually in greater quantities than that of the average consumer wholesale and retail buyers Buyers who purchase goods for resale. consignment buying A buying process in which goods are paid for only after the final customer purchases them. memorandum buying The buying process in which the supplier agrees to take back any unsold goods by a pre-established date. |

OB 3 Explain the process of purchasing (e.g., information gathering, open-to-buy, selecting suppliers)

Most purchasing specialists conduct a standard purchasing process to buy goods and services for their businesses. This process typically consists of identifying company needs, searching for and selecting suppliers, placing orders, and evaluating supplier performance. open-to-buy (OTB) The amount of money a retailer has left for buying goods after considering all purchases received, on order, and in transit.

The process usually starts with a demand or requirements – this could be for a physical part (inventory) or a service. A requisition is generated, which details the requirements (in some cases providing a requirements speciation) which actions the procurement department. A request for proposal (RFP) or request for quotation (RFQ) is then raised. Suppliers send their quotations in response to the RFQ, and a review is undertaken where the best offer (typically based on price,availability and quality) is given the purchase order. Purchase orders (PO) can be of various types,including:

|

formula cheat sheet

Financial Analysis Instructional Unit

- Assets - Liabilites = networth

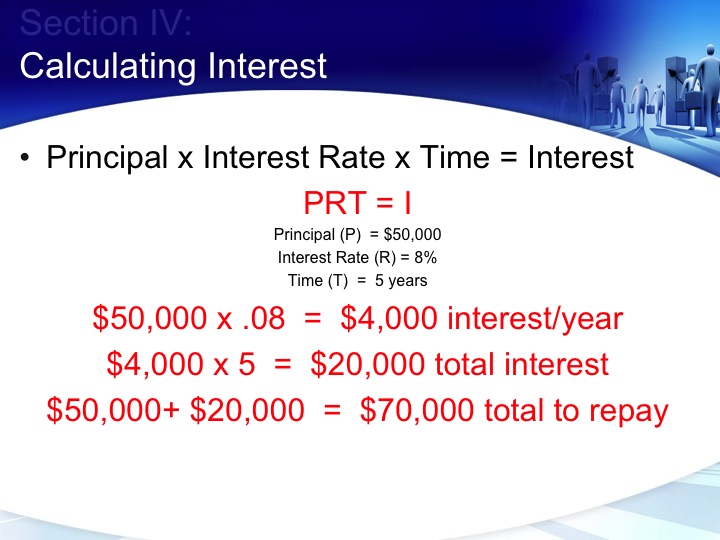

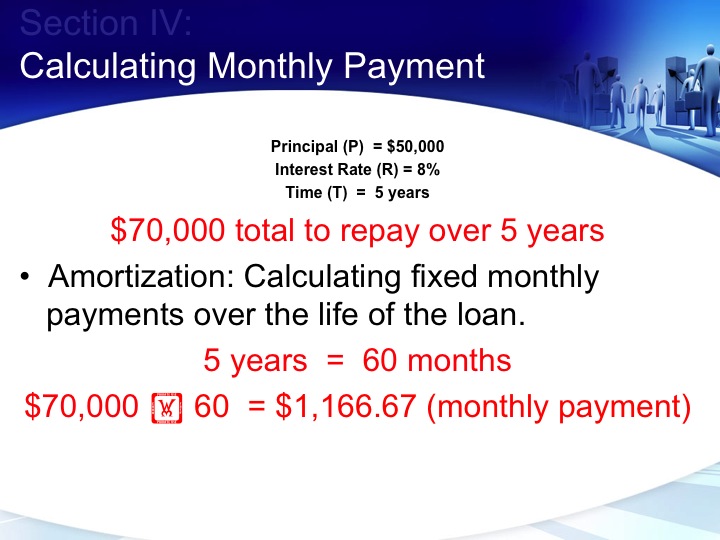

- Interest to pay = Principal x rate x time

- COGS = beg inventory + purchased inventory - ending inventory

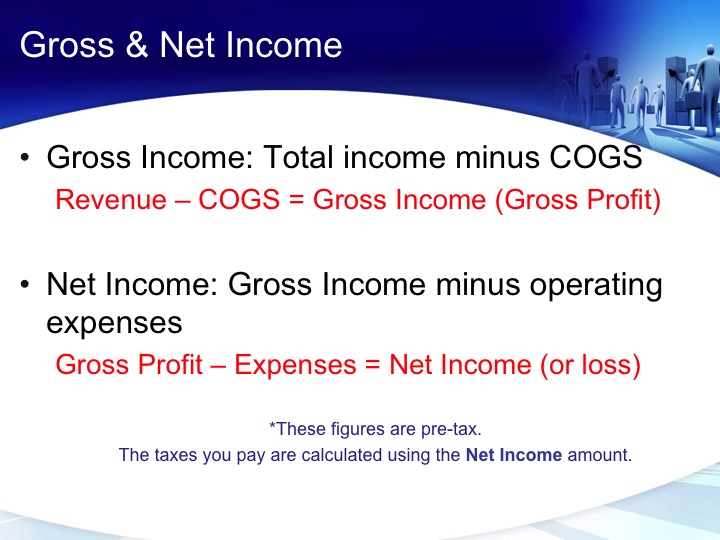

- Net income = gross profit - expenses

- Gross profit = revenue - cogs

- company’s gross profit is the revenue it makes after subtracting the costs of the products it has sold. For example, if a company made $1 million last quarter and spent $200,000 producing its goods, its gross profit is $800,000.

Financial Analysis Instructional Unit

OB 7 Explain the use of various business records (i.e., income statement, balance sheet, sales records, employment records)

Business financial records

Types of Accounts include

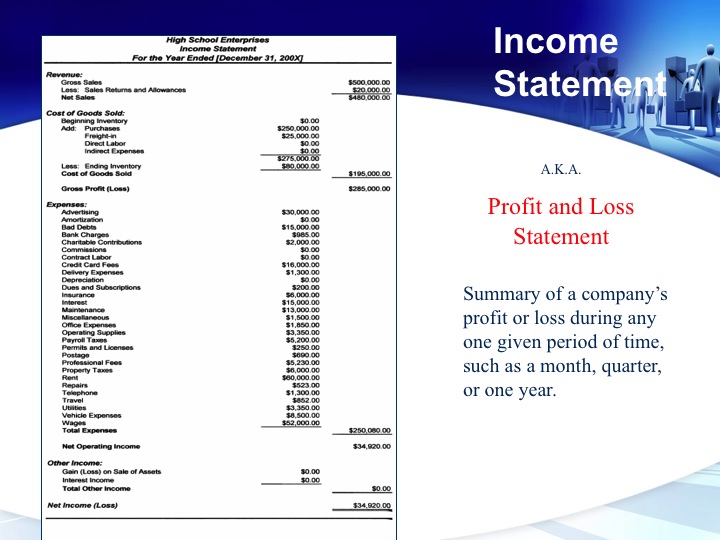

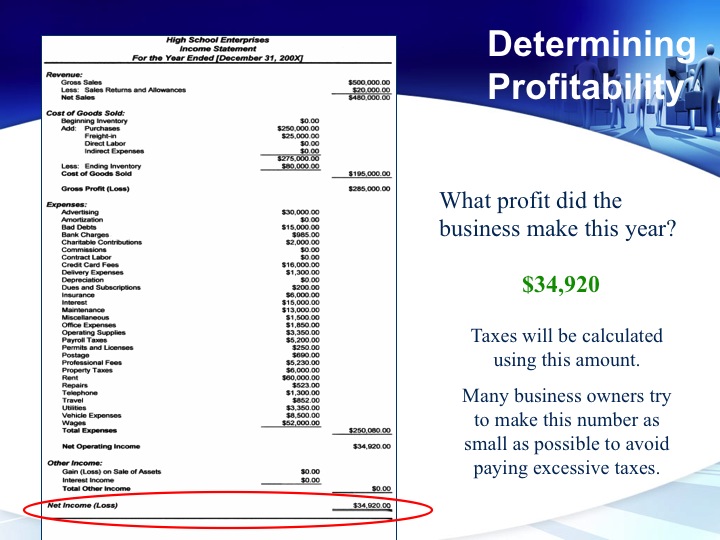

An income statement is a summary of a business’s income and expenses over a period of time. Simply put, it summarizes where the business’s money came from and where it went. It is a financial picture that lists all revenues and expenses for a certain time period, usually one year.

The income statement has many aliases. For instance, it is sometimes called an earnings statement. This name can be a bit deceiving, though, because even if a business is earning income, it isn’t necessarily earning a profit. Profit is the income left over once all expenses are paid. The income statement is the only financial statement that enables the business to look at its “bottom line.”

Traditionally, the income statement was referred to as the profit-and-loss statement, for obvious reasons—it shows a business’s profit and loss. The basic calculation used to analyze an income statement is “income minus expenses.” If the outcome is positive, the business has a profit. If the outcome is negative, the business has a loss. Over time, however, income statement has become the common business term for this important summary.

No matter what you call it, an income statement has at least five main categories. They include the following:

• Revenue

• Cost of goods sold/Cost of sales

• Gross profit

• Operating expenses

• Net income/profit

Revenue. Revenue is the total amount of money earned by a business. It includes sales of the business’s goods and services, interest earned from bank accounts, returns on investments, and

the sale of the business’s assets. All money coming in to the business, no matter what the source,

is revenue.

Think about how many different kinds of businesses exist and all the different ways there are to earn revenue. Some businesses sell services, while others sell goods. Hotels and resorts earn revenue by providing lodging and conference rooms for guests. Manufacturers such as the Ford Motor Company earn revenue by selling cars. What other examples can you think of?

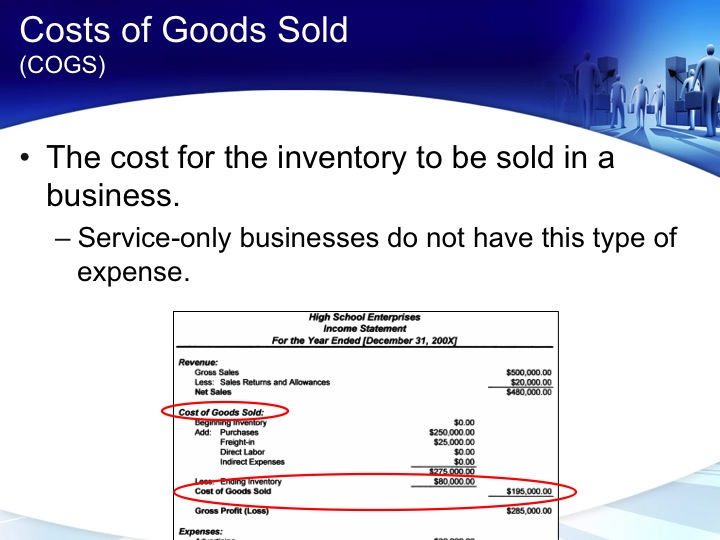

Cost of goods sold/Cost of sales. This element of the income statement includes all direct costs to obtain and/or produce the goods or services that a business sells. This includes:

• Raw materials

• Manufacturing overhead

• Packaging

• Shipping

• Labor

• Supplies

• Unsold items

• Stolen items

• Returned items

Although all businesses have costs, different businesses have different kinds of costs. When you look at the list above, can you determine which costs are associated with manufacturers, which are associated with retailers, and which are associated with service providers? Manufacturers have costs associated with making a product. Most manufacturing firms list these expenses on their income statements as “cost of goods sold.” Retailers have costs associated with obtaining goods from others and reselling them to ultimate users, while service providers are concerned with all costs directly associated with providing their services. Retailers and service providers usually list these expenses on their income statements as “cost of sales.”

Gross profit. Businesses use the term “gross” when they are looking at a total sum of money. Gross profit is determined by subtracting the cost of goods sold from revenue. It is the total profit made before all other remaining expenses have been deducted. For example, you don’t take operating expenses into account when calculating gross profit. Determining the gross profit helps businesses to see how much money they’ve invested in making or obtaining their products versus how much it costs to run the business. In this way, businesses are able to see what is costing the most money and can target trouble areas more effectively.

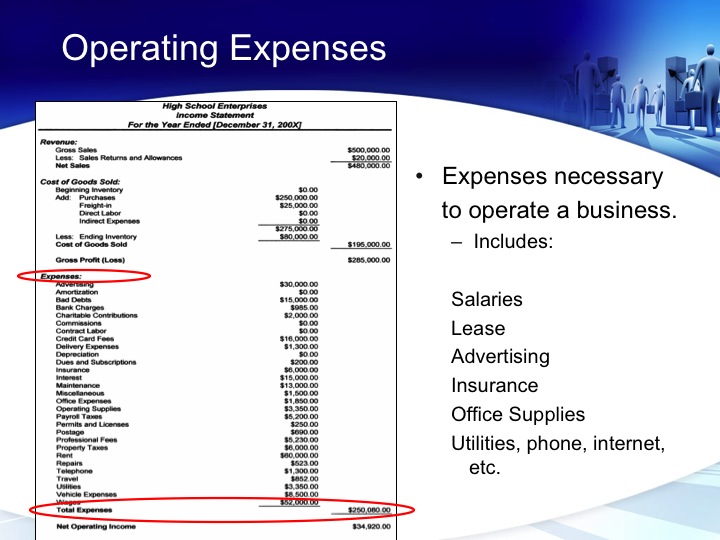

Operating expenses. This element of the income statement addresses all other expenses associated with the business, including:

• Employee wages/salaries

• Advertising

• Insurance

• Utilities (natural gas, electricity, water, etc.)

• Mortgage or rent

• Administrative costs

• Interest paid on outstanding loans

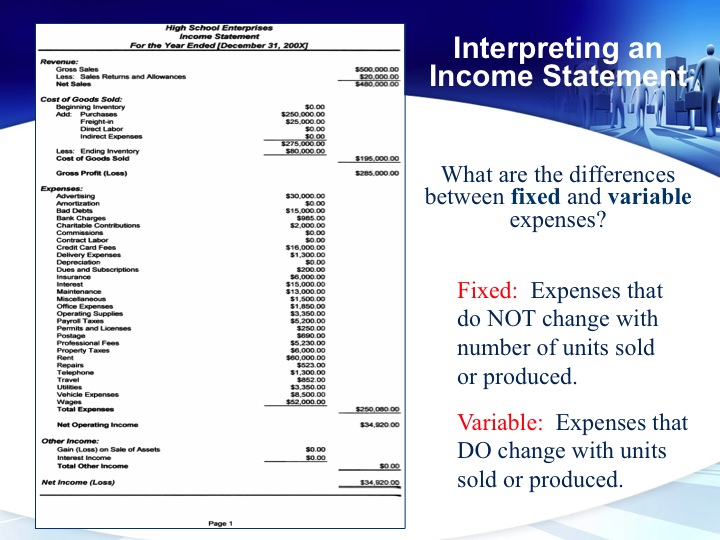

These are the expenses incurred from keeping a business’s doors open. The business pays these expenses so it can operate. Operating expenses may be either variable (amounts that are constantly changing, such as advertising costs) or fixed (amounts that stay the same for long periods of time, such as rent).

Net income--the “bottom line.” Here is where it gets exciting—net income is the business’s final profit. This is the money the company actually makes after all expenses have been deducted and taxes have been paid. As you might guess, net income is usually considered the most important item on the income statement—because it answers the question, “Is this business profitable?” Net income is sometimes called net profit or net earnings. The accuracy of this “bottom line” depends on the accuracy of reported revenues and expenses. Since the income statement not only determines final profit but is also used to develop other financial documents, it must be as accurate as possible. Without an accurate income statement, a company can face serious consequences!

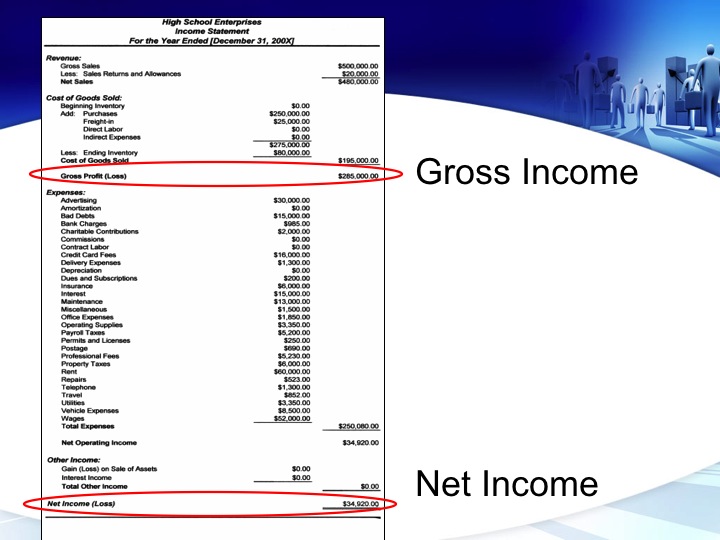

The income statement This picture is cumulative. This means that each income statement represents a total for a specific time period, usually one year (although income statements can be produced for quarters or months if desired).

Income Statement – summarizes the business’s income and expenses during a specified time period. Shows a business’s total financial picture—the good, the bad, and the ugly.Basic calculations for an income statement are

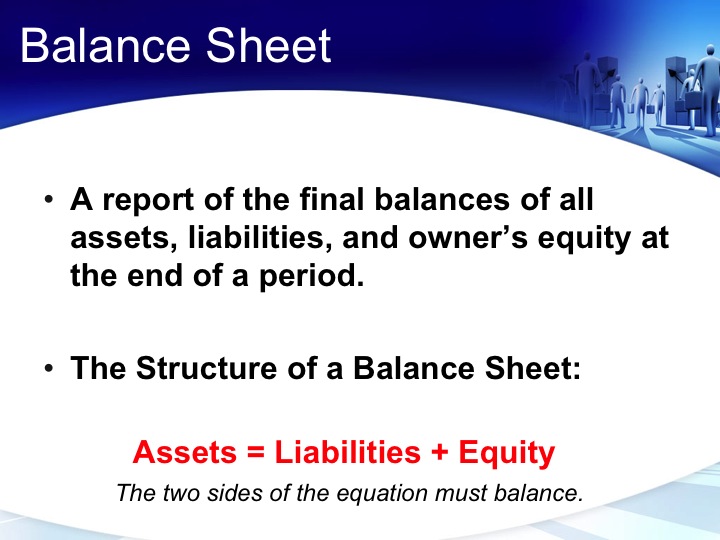

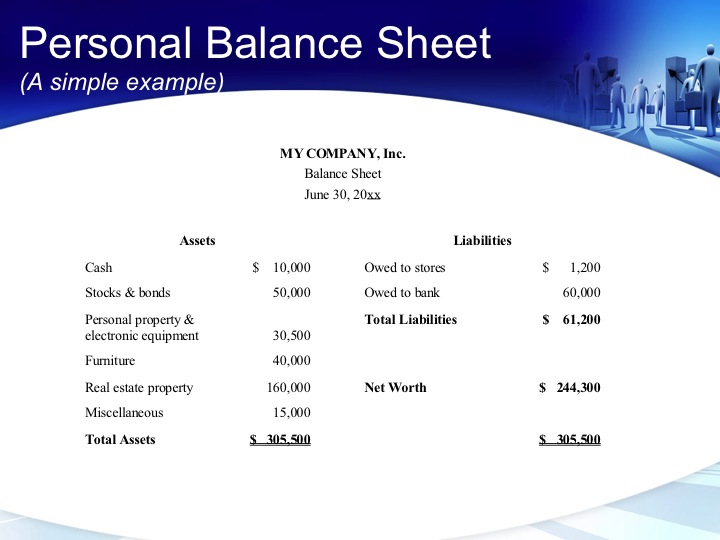

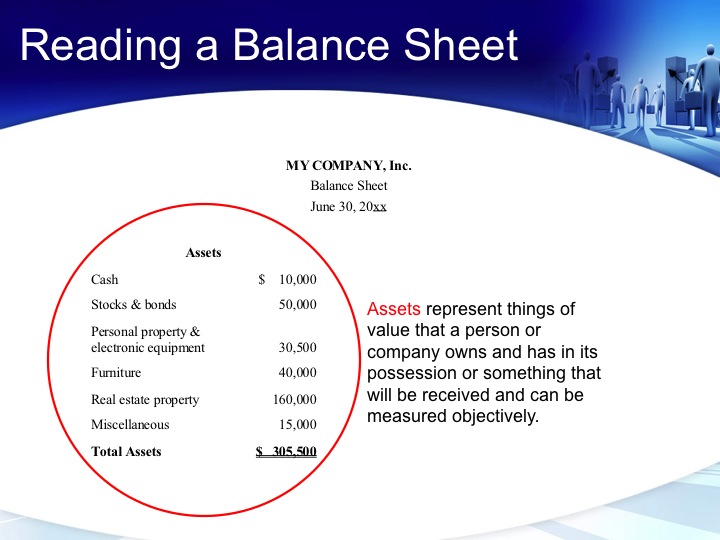

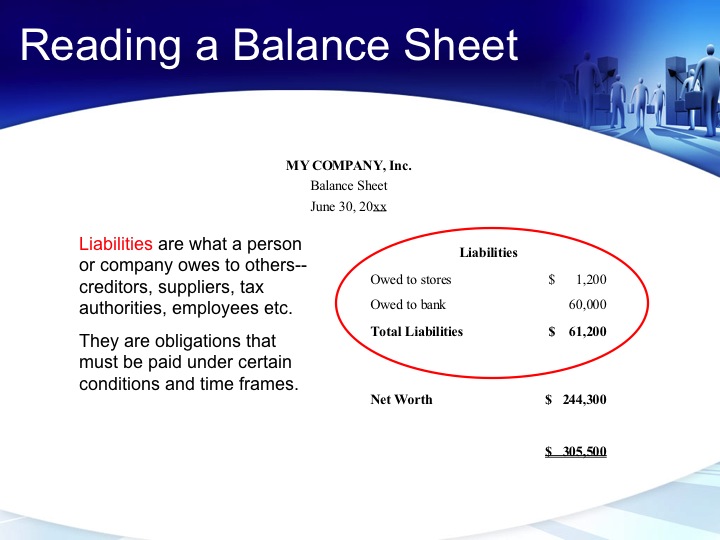

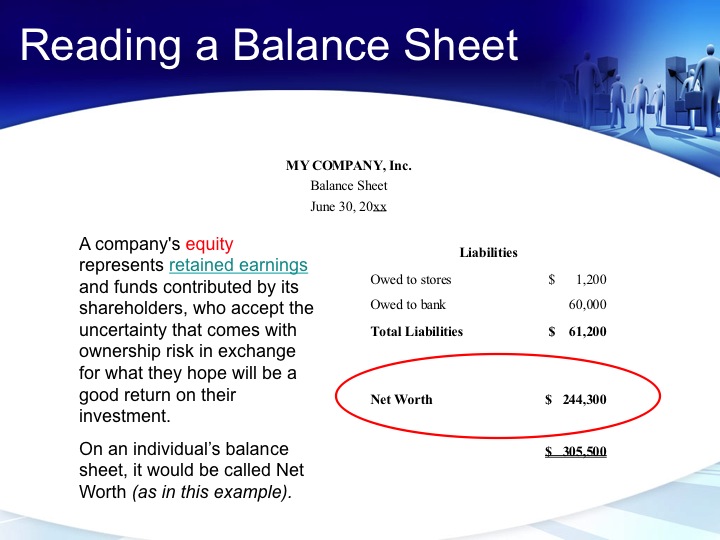

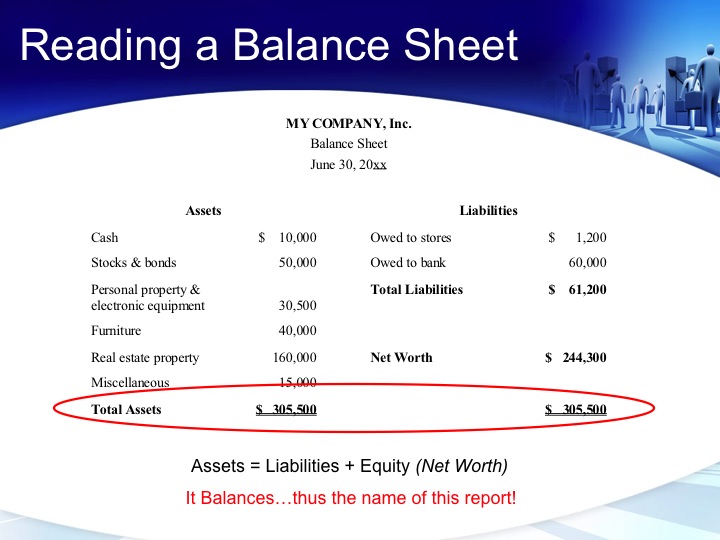

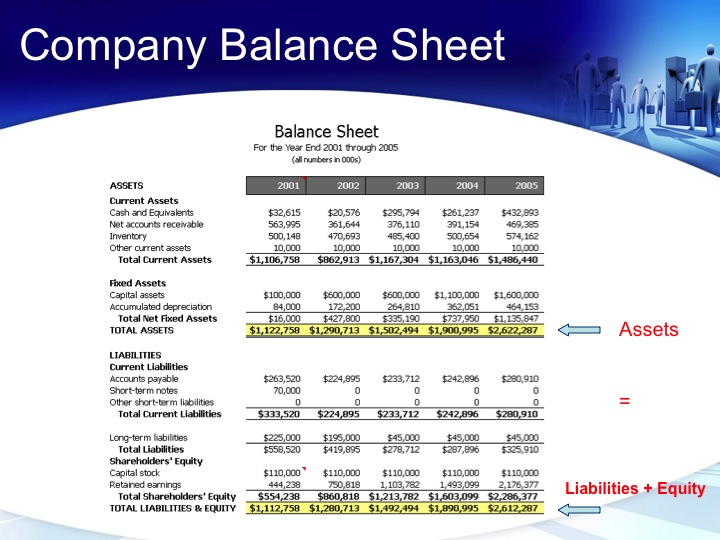

Balance Sheet

Balance Sheet – the summary of a business’s assets and liabilities. Indicates the financial condition of the business.

Daily Transactions

Sales Tally – a calculation of the daily sales

Sales Reports

Uses of Sales Reports is important to a business in the following decisions

Auditing

Auditing – the process that ensures the accuracy of a business’s finances

Identifying Discrepancies – identifies errors

Protecting the Business – from dishonest employees

Verifying Accuracy

OB 5 Calculate net sales

net sales - the amount left after gross sales have been adjusted for returns and allowances

gross sales - returns and allowances = net sales

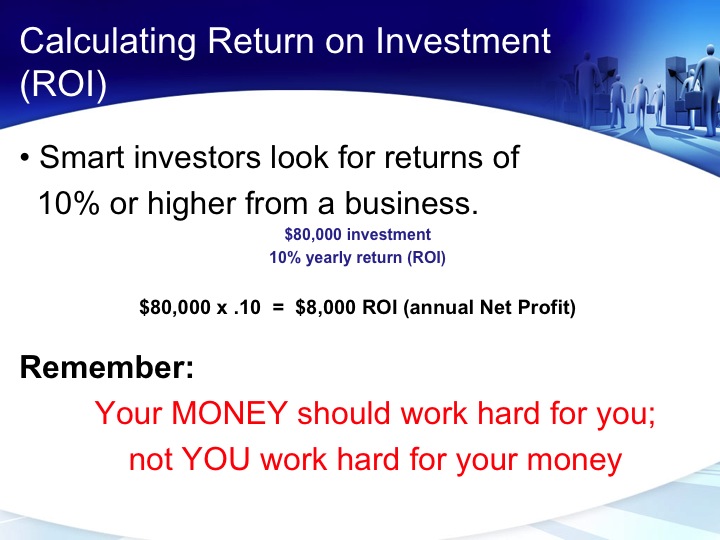

Return on Investment

(ROI)Return on Investment (ROI) or Return on Marketing Investment (ROMI) equals the gain from a program minus the cost of the program, divided by the cost of the program.

ROI = (gain - cost) / cost

For example: Let's assume that you started a new (incremental) advertising program, that it cost $50,000 in its first year, that it promoted $600,000 in incremental sales during the same year, and that the gross profit from these sales was $200,000.

If you subtract your incremental advertising dollars ($50,000) from the incremental gross profit generated ($200,000), you see that you have generated $150,000 of net operating profit.

Stated differently: the effect of your advertising added $200,000 to operating profit, and the cost of your advertising subtracted $50,000 from operating profit, for a net increase of $150,000.

Your ROI is ($200,000 - $50,000) / $50,000 = 3 = 300 percent

In other words, on average, each dollar you spent on the new (incremental) program brought in three dollars of profit. Usually ROI is expressed as a percentage.

Payroll - hours worked X rate of pay - deductions = paycheck...

http://www.metrojoe.org/Metrojoe_Interactive_Guide/Chapter_3/Chapter3_LessonPlans/Chapter3_LessonPlan2.pdf

In general, follow these steps to calculate the amount of overtime pay owed to an employee:

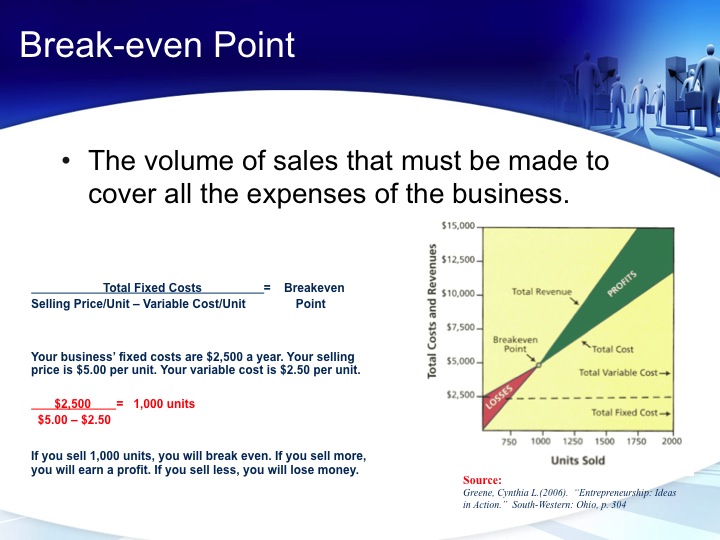

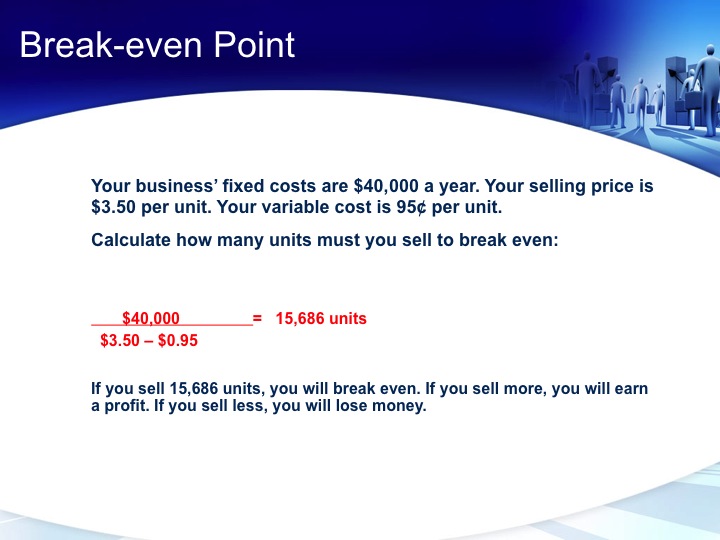

BREAK EVEN POINT

A company reaches its breakeven point when total expenses equal total sales. At this point, the business has covered its costs but has not yet made a profit. The formula for calculating breakeven point is:

Fixed costs / (Price per unit- Variable costs per unit) = Breakeven point

Example: A company incurs a total of $20,000 in fixed costs, and each product carries $3 in variable costs. If the company sells each product for $10, it will break even after selling 2,858 products: $20,000 / ($10 - $3) = 2,858.

Operating Expenses or Overhead

Every business has operating costs. There are a few different terms that may be used to describe these costs, such as “overhead” or “OPEX” (operating expenses). No matter what they’re called, these are the ongoing, day-to-day expenses of running a business that are not directly related to production.

The two main types of operating costs are fixed and variable

1. Operating costs that do not increase or decrease with changes in production are called fixed expenses

· Advertising and promotion

Example: A company ramps up its production of pool accessories for the summer. During this season, it spends more on advertising and promotion to keep sales moving.

· Travel expenses

Example: A company has slowed down its production of medical supplies due to lower demand. This also means that the company is spending less on travel expenses for its sales associates, as they are now visiting accounts just once a month, instead of twice.

· Sales commissions

Example: Demand for flat-screen televisions is up during the holiday season, so an electronics manufacturer is producing more of them. Its sales associates are selling more televisions to wholesalers and retailers, meaning their commissions have been higher lately.

· Employee bonuses

Example: A financial-services firm has had a stellar year selling its products (e.g., retirement-plan administration, investment advising, etc.) to more customers than ever. As a result, its employees will be receiving larger bonuses this year.

· Certain permits and fees

Example: As the economy recovers and more people build new homes, a construction business has more customers and is paying more in building permits and fees.

· Costs of providing free shipping, delivery, or installation

Example: An appliance manufacturer offers free delivery to wholesalers and retailers who spend a certain amount of money with each order. Demand for appliances is up, so the manufacturer has been producing more, customers have been ordering more, and—as a result—the costs of providing free delivery have risen as well.

Business financial records

Types of Accounts include

- Accounts Receivable – money owed to a business by its customers

- Accounts Payable – money owed to a vendor for merchandise, equipment, or other supplies

- Purchase Order – a written form authorizing vendors to ship products at a specified price

- Cash Receipts – any cash brought into the business

- Cash Disbursements – any cash paid out by the business

An income statement is a summary of a business’s income and expenses over a period of time. Simply put, it summarizes where the business’s money came from and where it went. It is a financial picture that lists all revenues and expenses for a certain time period, usually one year.

The income statement has many aliases. For instance, it is sometimes called an earnings statement. This name can be a bit deceiving, though, because even if a business is earning income, it isn’t necessarily earning a profit. Profit is the income left over once all expenses are paid. The income statement is the only financial statement that enables the business to look at its “bottom line.”

Traditionally, the income statement was referred to as the profit-and-loss statement, for obvious reasons—it shows a business’s profit and loss. The basic calculation used to analyze an income statement is “income minus expenses.” If the outcome is positive, the business has a profit. If the outcome is negative, the business has a loss. Over time, however, income statement has become the common business term for this important summary.

No matter what you call it, an income statement has at least five main categories. They include the following:

• Revenue

• Cost of goods sold/Cost of sales

• Gross profit

• Operating expenses

• Net income/profit

Revenue. Revenue is the total amount of money earned by a business. It includes sales of the business’s goods and services, interest earned from bank accounts, returns on investments, and

the sale of the business’s assets. All money coming in to the business, no matter what the source,

is revenue.

Think about how many different kinds of businesses exist and all the different ways there are to earn revenue. Some businesses sell services, while others sell goods. Hotels and resorts earn revenue by providing lodging and conference rooms for guests. Manufacturers such as the Ford Motor Company earn revenue by selling cars. What other examples can you think of?

Cost of goods sold/Cost of sales. This element of the income statement includes all direct costs to obtain and/or produce the goods or services that a business sells. This includes:

• Raw materials

• Manufacturing overhead

• Packaging

• Shipping

• Labor

• Supplies

• Unsold items

• Stolen items

• Returned items

Although all businesses have costs, different businesses have different kinds of costs. When you look at the list above, can you determine which costs are associated with manufacturers, which are associated with retailers, and which are associated with service providers? Manufacturers have costs associated with making a product. Most manufacturing firms list these expenses on their income statements as “cost of goods sold.” Retailers have costs associated with obtaining goods from others and reselling them to ultimate users, while service providers are concerned with all costs directly associated with providing their services. Retailers and service providers usually list these expenses on their income statements as “cost of sales.”

Gross profit. Businesses use the term “gross” when they are looking at a total sum of money. Gross profit is determined by subtracting the cost of goods sold from revenue. It is the total profit made before all other remaining expenses have been deducted. For example, you don’t take operating expenses into account when calculating gross profit. Determining the gross profit helps businesses to see how much money they’ve invested in making or obtaining their products versus how much it costs to run the business. In this way, businesses are able to see what is costing the most money and can target trouble areas more effectively.

Operating expenses. This element of the income statement addresses all other expenses associated with the business, including:

• Employee wages/salaries

• Advertising

• Insurance

• Utilities (natural gas, electricity, water, etc.)

• Mortgage or rent

• Administrative costs

• Interest paid on outstanding loans

These are the expenses incurred from keeping a business’s doors open. The business pays these expenses so it can operate. Operating expenses may be either variable (amounts that are constantly changing, such as advertising costs) or fixed (amounts that stay the same for long periods of time, such as rent).

Net income--the “bottom line.” Here is where it gets exciting—net income is the business’s final profit. This is the money the company actually makes after all expenses have been deducted and taxes have been paid. As you might guess, net income is usually considered the most important item on the income statement—because it answers the question, “Is this business profitable?” Net income is sometimes called net profit or net earnings. The accuracy of this “bottom line” depends on the accuracy of reported revenues and expenses. Since the income statement not only determines final profit but is also used to develop other financial documents, it must be as accurate as possible. Without an accurate income statement, a company can face serious consequences!

The income statement This picture is cumulative. This means that each income statement represents a total for a specific time period, usually one year (although income statements can be produced for quarters or months if desired).

Income Statement – summarizes the business’s income and expenses during a specified time period. Shows a business’s total financial picture—the good, the bad, and the ugly.Basic calculations for an income statement are

- Net Sales = Total Sales – Sales Returns and Allowances

- Gross Profit = Net Sales – Cost of Goods Sold

- Net Income before Taxes = Gross Profit – Operating Expenses

- Net Income = Net Income before Taxes – Taxes

- Total Sales – Total amount received from the sales for a business

- Sales Returns and Allowances – the credit granted to customers who have returned a damaged or unwanted good

- Cost of Goods Sold – the cost to either manufacture or buy the merchandise to be sold

- Operating Expenses – the costs incurred from operating the business which can include wages or rent

- Variable expenses – change monthly

- Fixed expenses – stay the same no matter the level of production

- Income Taxes

- Net Income – income earned after deducting sales returns and allowances, cost of goods sold, operating expenses, and income taxes from sales

Balance Sheet

Balance Sheet – the summary of a business’s assets and liabilities. Indicates the financial condition of the business.

- Asset – anything of value that the business owns

- Liability – the amount of money the business owes

- Net Worth = Assets - Liabilities

Daily Transactions

Sales Tally – a calculation of the daily sales

- Can be used to compare a store’s performance from year to year

- Provides up-to-date information about what is selling and not selling

- Allows the business to catch any discrepancies on a daily basis

- Deposits should be made daily to ensure that large sums of money are not left in the store

Sales Reports

Uses of Sales Reports is important to a business in the following decisions

- Merchandising Decisions

- Pricing Decisions

- Purchasing Decisions

- Sales Quotas – a sales goal

- Scheduling of employees

- Total Sales

- Department Sales

- Product Sales

- Average Dollar Sale

- Average Units per Transaction

- Hourly Sales

- Goals

Auditing

Auditing – the process that ensures the accuracy of a business’s finances

Identifying Discrepancies – identifies errors

Protecting the Business – from dishonest employees

Verifying Accuracy

OB 5 Calculate net sales

net sales - the amount left after gross sales have been adjusted for returns and allowances

gross sales - returns and allowances = net sales

Return on Investment

(ROI)Return on Investment (ROI) or Return on Marketing Investment (ROMI) equals the gain from a program minus the cost of the program, divided by the cost of the program.

ROI = (gain - cost) / cost

For example: Let's assume that you started a new (incremental) advertising program, that it cost $50,000 in its first year, that it promoted $600,000 in incremental sales during the same year, and that the gross profit from these sales was $200,000.

If you subtract your incremental advertising dollars ($50,000) from the incremental gross profit generated ($200,000), you see that you have generated $150,000 of net operating profit.

Stated differently: the effect of your advertising added $200,000 to operating profit, and the cost of your advertising subtracted $50,000 from operating profit, for a net increase of $150,000.

Your ROI is ($200,000 - $50,000) / $50,000 = 3 = 300 percent

In other words, on average, each dollar you spent on the new (incremental) program brought in three dollars of profit. Usually ROI is expressed as a percentage.

Payroll - hours worked X rate of pay - deductions = paycheck...

http://www.metrojoe.org/Metrojoe_Interactive_Guide/Chapter_3/Chapter3_LessonPlans/Chapter3_LessonPlan2.pdf

In general, follow these steps to calculate the amount of overtime pay owed to an employee:

- Determine whether the individual is eligible for overtime. ...

- Determine the hourly rate of pay, which is the total amount paid in the period divided by the number of hours worked.

- Multiply the hourly rate of pay by 1.5x

BREAK EVEN POINT

A company reaches its breakeven point when total expenses equal total sales. At this point, the business has covered its costs but has not yet made a profit. The formula for calculating breakeven point is:

Fixed costs / (Price per unit- Variable costs per unit) = Breakeven point

Example: A company incurs a total of $20,000 in fixed costs, and each product carries $3 in variable costs. If the company sells each product for $10, it will break even after selling 2,858 products: $20,000 / ($10 - $3) = 2,858.

Operating Expenses or Overhead

Every business has operating costs. There are a few different terms that may be used to describe these costs, such as “overhead” or “OPEX” (operating expenses). No matter what they’re called, these are the ongoing, day-to-day expenses of running a business that are not directly related to production.

The two main types of operating costs are fixed and variable

1. Operating costs that do not increase or decrease with changes in production are called fixed expenses

- Janitorial services, Trash removal, Lawn care

- Utilities (electricity, gas, water, sewage, etc.)

- Insurance

- Property taxes

- Rent/Mortgage

- Wages/Salaries

- Employee benefits: Health insurance, Retirement, Vacation

- Office supplies

- Office equipment (computers, copiers, etc.)

- Certain business services, such as accounting, legal, etc.

- Depreciation (loss of value on certain company property, such as computers or vehicles)

· Advertising and promotion

Example: A company ramps up its production of pool accessories for the summer. During this season, it spends more on advertising and promotion to keep sales moving.

· Travel expenses

Example: A company has slowed down its production of medical supplies due to lower demand. This also means that the company is spending less on travel expenses for its sales associates, as they are now visiting accounts just once a month, instead of twice.

· Sales commissions

Example: Demand for flat-screen televisions is up during the holiday season, so an electronics manufacturer is producing more of them. Its sales associates are selling more televisions to wholesalers and retailers, meaning their commissions have been higher lately.

· Employee bonuses

Example: A financial-services firm has had a stellar year selling its products (e.g., retirement-plan administration, investment advising, etc.) to more customers than ever. As a result, its employees will be receiving larger bonuses this year.

· Certain permits and fees

Example: As the economy recovers and more people build new homes, a construction business has more customers and is paying more in building permits and fees.

· Costs of providing free shipping, delivery, or installation

Example: An appliance manufacturer offers free delivery to wholesalers and retailers who spend a certain amount of money with each order. Demand for appliances is up, so the manufacturer has been producing more, customers have been ordering more, and—as a result—the costs of providing free delivery have risen as well.